Special Development Areas Act

By Terra Caribbean on 07 Sep, 2018

The Special Development Areas Act sets out the designation of special development areas and provides relief for approved developers constructing or improving a building or structure in those areas and to persons financing such work (other than a commercial bank).

The activities that an approved developer may carry out are:

- Hotels including conference areas;

- Residential complexes;

- Commercial or industrial buildings including office complexes;

- Other tourism facilities;

- Water-based activities;

- Tourism projects highlighting heritage and natural environment;

- Arts and cultural investments; and

- Agricultural-based activities.

Exemptions & Allowances

Approved developers are exempt from:

- Import duties and VAT on inputs for the construction or renovation of buildings and refurbishment of existing buildings.

- Charges on repatriation of interest (for a period of 10 years),

- Land tax on the improved value of the land

- Property transfer tax payable by vendors on the initial purchase of the property whether national or non-national

Persons financing such work are exempt from:

• Income tax on interest earned on loans to approved developer.

Allowances

- An approved developer pays Corporate Income Tax (CIT) at the rate of 15%

- Is granted initial allowances of 40% and annual allowances of 6% on industrial buildings

- Is granted initial allowances of 20% and annual allowances of 4% on commercial buildings.

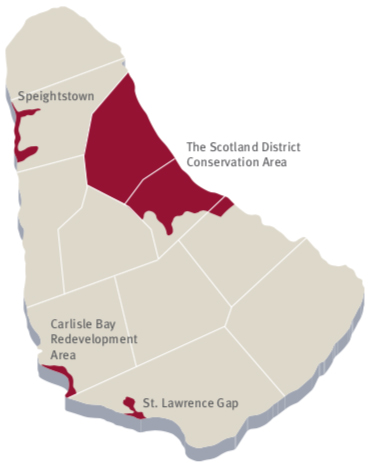

DEFINED AREAS

The areas which are currently defined as development areas:

- Carlisle Bay Redevelopment area in St. Michael;

- Speightstown in St. Peter;

- St. Lawrence Gap in Christ Church; and

- The Scotland District Conservation Area.

For more details on the Special Development Areas Act please refer to CAP 237A- Special development Areas Act